Your credit score is a three-digit figure that gives lenders an idea of your overall credit health, and this metric can be a lot more important than people realize. After all, you typically need good credit to rent an apartment or qualify for a rewards credit card, and information on your credit reports may be requested by employers before they hire you for a job. Good credit can also help you secure a mortgage or the best auto loans, whereas a bad credit score can prevent you from qualifying at all.

Fortunately, there are standard steps to take if you want to keep your credit score in good shape. For example, paying all your bills on time and keeping your credit utilization in check can go a long way toward helping you build the credit you’ll need later in life. In the meantime, you’ll also want to check your credit reports for incorrect reporting and false information, all of which can negatively impact your score without you even knowing.

Just remember that having negative items removed from your credit reports only works if they are actually untrue. The CFPB points this out very specifically on their website:

“You generally cannot have negative but accurate information removed from your credit report,” they write, adding that most negative information will remain on your credit reports for seven years.

In addition to checking your credit reports for errors, you should have a general idea of how credit scores are calculated. You probably have additional questions you want answered as well.

For example, what is a good credit score? And what is a bad credit score?

First off, you should know that the most important credit scoring model is the FICO scoring. Meanwhile, VantageScore is the second most commonly used credit scoring model.

Since FICO credit scores are used by 90% of top lenders, we’ll focus on this type of credit score for the purpose of this guide. Like VantageScore, FICO credit scores fall between 300 and 850, with higher scores being superior to lower credit scores.

According to myFICO.com, FICO credit scores are also separated into the following ranges:

If you’re wondering where you stand, you should know that Experian reported that the average FICO score came in at 714 in 2022. This means that, for the time being, most American consumers have what is considered a “good” credit score.

To keep your credit score in the best possible shape, you should make sure you read over your credit reports from all three credit bureaus — Experian, Equifax, and TransUnion — at least a few times each year. Doing so can help you spot inconsistencies in your credit reports and even false reporting or mistakes.

According to the Federal Trade Commission (FTC), checking your credit reports is also one way to spot signs of identity theft early in the process.

To get a look at your credit reports from all three bureaus, you should use the website AnnualCreditReport.com. This portal lets you check all of your credit reports for free up to once per week, and you can complete the entire process online.

If you find any errors on your credit reports, especially errors that may be hurting your score, you should take steps to have them removed. Just remember that you will only have success having negative reporting removed from your reports if the information is actually incorrect.

The FTC notes that you’ll need to dispute any incorrect reporting with both the credit bureaus that report the information and the company that supplied the data. If your Experian credit report shows a late payment on your Wells Fargo car payment, for example, you would need to dispute the information with both Experian and Wells Fargo.

If the false information was on all three of your credit reports, on the other hand, you would need to send the same information to Experian, Equifax, TransUnion, and Wells Fargo.

Steps you’ll need to take to dispute information on your credit reports include:

Note that you can put together a single packet of this information and send it to the credit bureaus and the company that reported the information. In some cases, however, credit bureaus also have their own dispute form you can send along.

If you’re not disputing information on your credit reports online, make sure to send the information for your dispute via certified mail.

Either way, you’ll want to send the information to the appropriate credit bureau using the information below, and you can send the information to the reporting company using the address listed on your credit report.

If all of this sounds overwhelming, it’s also worth mentioning that the best credit repair companies can take on this work for you. Not only can these companies pore over your credit reports to check for errors, but they can dispute errors and misreporting on your behalf.

For example, Lexington Law charges reasonable fees in exchange for handling all aspects of credit repair ranging from disputing incorrect information on your credit reports to bankruptcies, collections, foreclosures, and more. The company also lets you complete the entire process online and over the phone, so you won’t have to drive to a credit repair office or spend time meeting with someone in person.

While it’s possible almost anything on your credit report could be a mistake, the Consumer Financial Protection Bureau (CFPB) says the following credit report errors are some of the most common:

Any of these errors could be hurting your credit score in some way, which is totally avoidable if you take steps to dispute incorrect data. If you’ve been wondering how to build your credit score, this is one move you’ll want to make at least a few times per year.

Related: How to Raise Your Credit in 5 Months

If you want to improve your credit score so you can qualify for a mortgage, a car loan, or the best personal loans and credit cards, you should make sure you check your credit reports every few months. Doing so can help you discover errors before they cause too much damage, and you can also spot the early signs of identity theft.

Simply put, there are no downsides that come with checking your credit reports for free and disputing false items. If you fail to do so, however, you could live to regret it.

You can get something taken off your credit report by contacting the credit bureau that is reporting it. You will need to provide proof that the item is incorrect or outdated. The bureau will then investigate and may remove the item from your credit report.

What information can’t be disputed from my credit report?

The following information cannot be disputed from your credit report: the name of the creditor, the account number, the date of the last activity on the account, and the credit limit.

Can I legally remove things from your credit report?

Yes, you can legally remove things from your credit report. You can also dispute inaccurate or incomplete information on your credit report.

The post How to Remove Negative Items From Your Credit Reports appeared first on Good Financial Cents®.

Fortunately, there are standard steps to take if you want to keep your credit score in good shape. For example, paying all your bills on time and keeping your credit utilization in check can go a long way toward helping you build the credit you’ll need later in life. In the meantime, you’ll also want to check your credit reports for incorrect reporting and false information, all of which can negatively impact your score without you even knowing.

Just remember that having negative items removed from your credit reports only works if they are actually untrue. The CFPB points this out very specifically on their website:

“You generally cannot have negative but accurate information removed from your credit report,” they write, adding that most negative information will remain on your credit reports for seven years.

Table of Contents

- How Credit Scores Are Calculated

- What to Do If You Find Something Wrong in Your Reports

- How to Dispute Negative Items on Your Credit Reports

- Credit Bureau Dispute Information

- Common Credit Report Errors and Entries That Hurt the Most

- Final Thoughts on Removing Negative Items From Your Credit

- FAQs on Removing Negative Items on Credit Reports

How Credit Scores Are Calculated

In addition to checking your credit reports for errors, you should have a general idea of how credit scores are calculated. You probably have additional questions you want answered as well.

For example, what is a good credit score? And what is a bad credit score?

First off, you should know that the most important credit scoring model is the FICO scoring. Meanwhile, VantageScore is the second most commonly used credit scoring model.

Since FICO credit scores are used by 90% of top lenders, we’ll focus on this type of credit score for the purpose of this guide. Like VantageScore, FICO credit scores fall between 300 and 850, with higher scores being superior to lower credit scores.

According to myFICO.com, FICO credit scores are also separated into the following ranges:

- Exceptional: 800+

- Very Good: 740 to 799

- Good: 670 to 739

- Fair: 580 to 559

- Poor: 580 or less

If you’re wondering where you stand, you should know that Experian reported that the average FICO score came in at 714 in 2022. This means that, for the time being, most American consumers have what is considered a “good” credit score.

What to Do If You Find Something Wrong in Your Reports

To keep your credit score in the best possible shape, you should make sure you read over your credit reports from all three credit bureaus — Experian, Equifax, and TransUnion — at least a few times each year. Doing so can help you spot inconsistencies in your credit reports and even false reporting or mistakes.

According to the Federal Trade Commission (FTC), checking your credit reports is also one way to spot signs of identity theft early in the process.

To get a look at your credit reports from all three bureaus, you should use the website AnnualCreditReport.com. This portal lets you check all of your credit reports for free up to once per week, and you can complete the entire process online.

How to Dispute Negative Items on Your Credit Reports

If you find any errors on your credit reports, especially errors that may be hurting your score, you should take steps to have them removed. Just remember that you will only have success having negative reporting removed from your reports if the information is actually incorrect.

The FTC notes that you’ll need to dispute any incorrect reporting with both the credit bureaus that report the information and the company that supplied the data. If your Experian credit report shows a late payment on your Wells Fargo car payment, for example, you would need to dispute the information with both Experian and Wells Fargo.

If the false information was on all three of your credit reports, on the other hand, you would need to send the same information to Experian, Equifax, TransUnion, and Wells Fargo.

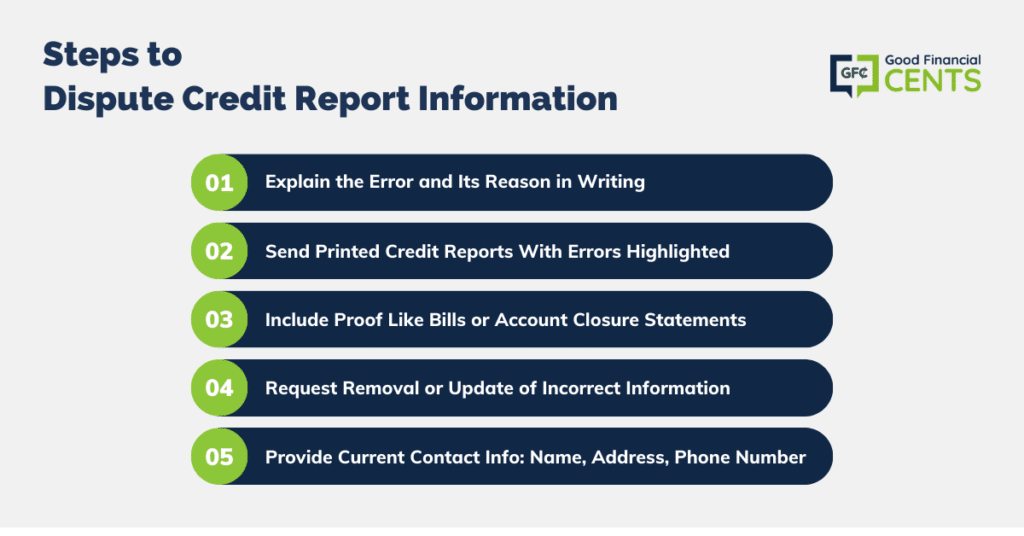

Steps you’ll need to take to dispute information on your credit reports include:

- Step 1: Explain in writing what you think is wrong on your credit reports, along with the reason the information is incorrect.

- Step 2: Send printed copies of your credit reports with your letter, and make sure to highlight or circle the incorrect information.

- Step 3: Include any proof you have that the information is wrong, such as a bill that shows your balances have been paid or an account closure statement.

- Step 4: Request in writing that the incorrect information you’re writing about is removed or updated.

- Step 5: Make sure to include up-to-date contact information for yourself when you contact each company, such as your name, address, and phone number.

Note that you can put together a single packet of this information and send it to the credit bureaus and the company that reported the information. In some cases, however, credit bureaus also have their own dispute form you can send along.

If you’re not disputing information on your credit reports online, make sure to send the information for your dispute via certified mail.

Either way, you’ll want to send the information to the appropriate credit bureau using the information below, and you can send the information to the reporting company using the address listed on your credit report.

Credit Bureau Dispute Information

| CREDIT BUREAU WEB PAGE | ADDRESSES FOR DISPUTES BY MAIL | PHONE NUMBER |

| Experian | Mail the Dispute Form With Your Letter to: ExperianP.O. Box 4500Allen, TX 75013 | (888) 397-3742 |

| Equifax | Download the Dispute Form and Mail Your Letter to: Equifax Information Services LLCP.O. Box 740256Atlanta, GA 30348 | (866) 349-5191 |

| TransUnion | Download the Dispute Form and Mail Your letter to: TransUnion LLCConsumer Dispute CenterP.O. Box 2000Chester, PA 19016 | (800) 916-8800 |

If all of this sounds overwhelming, it’s also worth mentioning that the best credit repair companies can take on this work for you. Not only can these companies pore over your credit reports to check for errors, but they can dispute errors and misreporting on your behalf.

For example, Lexington Law charges reasonable fees in exchange for handling all aspects of credit repair ranging from disputing incorrect information on your credit reports to bankruptcies, collections, foreclosures, and more. The company also lets you complete the entire process online and over the phone, so you won’t have to drive to a credit repair office or spend time meeting with someone in person.

Common Credit Report Errors and Entries That Hurt the Most

While it’s possible almost anything on your credit report could be a mistake, the Consumer Financial Protection Bureau (CFPB) says the following credit report errors are some of the most common:

- Wrong name or contact information

- Incorrect accounts that exist due to identity theft

- Closed accounts that are reported as open

- Accounts that are falsely reported as late or delinquent

- Incorrect dates for last payments

- Debts listed more than once

- Incorrect balances

- Incorrect credit reports

- Accounts with an incorrect credit limit

Any of these errors could be hurting your credit score in some way, which is totally avoidable if you take steps to dispute incorrect data. If you’ve been wondering how to build your credit score, this is one move you’ll want to make at least a few times per year.

Related: How to Raise Your Credit in 5 Months

Final Thoughts on Removing Negative Items From Your Credit

If you want to improve your credit score so you can qualify for a mortgage, a car loan, or the best personal loans and credit cards, you should make sure you check your credit reports every few months. Doing so can help you discover errors before they cause too much damage, and you can also spot the early signs of identity theft.

Simply put, there are no downsides that come with checking your credit reports for free and disputing false items. If you fail to do so, however, you could live to regret it.

FAQs on Removing Negative Items on Credit Reports

How do I get something taken off my credit report?You can get something taken off your credit report by contacting the credit bureau that is reporting it. You will need to provide proof that the item is incorrect or outdated. The bureau will then investigate and may remove the item from your credit report.

What information can’t be disputed from my credit report?

The following information cannot be disputed from your credit report: the name of the creditor, the account number, the date of the last activity on the account, and the credit limit.

Can I legally remove things from your credit report?

Yes, you can legally remove things from your credit report. You can also dispute inaccurate or incomplete information on your credit report.

The post How to Remove Negative Items From Your Credit Reports appeared first on Good Financial Cents®.